*shrug*JerryBoBerry said:don't like truth in visual form?

When it's done too often, it just makes the person come across as the crazy old homeless man with the "THE WORLD IS ENDING" sign.

*shrug*JerryBoBerry said:don't like truth in visual form?

PepperoniPiz said:I'd pay more attention to your posts if they weren't all just propaganda style images.

Bocefish said:Just Me said:How can you call something a failure that hasn't even taken affect yet?

Because it's foundation was based on on lies and it was passed because of more lies.

It's a failure because it forces insurers to cancel perfectly good plans that don't offer an “essential health benefits” package, providing coverage in 10 categories, including maternity, prescriptions, chronic disease management, mental health and pediatric services that many people don't need or want.

Why?

Because in 2011 the dept. of HHS found that 62% of enrollees didn’t have coverage for maternity services, 18% didn’t have coverage for mental health services and another 9% didn't have prescription coverage. Now people are mandated to pay way more for crap they don't need or want. Do you consider that a success?

I don't.

Forcing a one size fits all plan is BS.

As details emerge, you'll eventually figure out how bad it is, and it will only get worse.

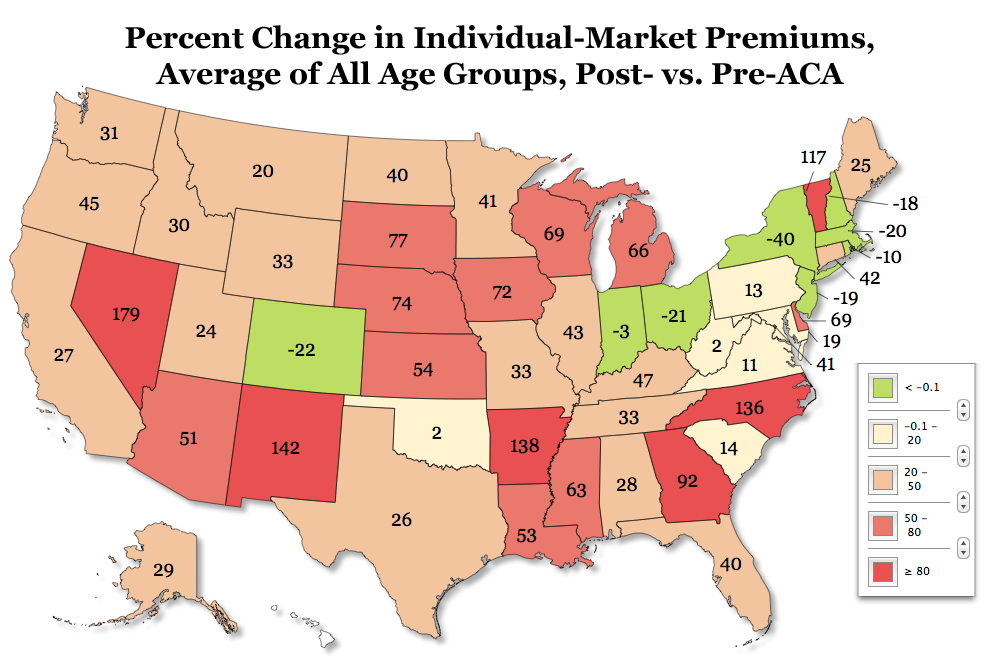

One of the fundamental flaws of the Affordable Care Act is that, despite its name, it makes health insurance more expensive. Today, the Manhattan Institute released the most comprehensive analysis yet conducted of premiums under Obamacare for people who shop for coverage on their own. Here’s what we learned. In the average state, Obamacare will increase underlying premiums by 41 percent. As we have long expected, the steepest hikes will be imposed on the healthy, the young, and the male. And Obamacare’s taxpayer-funded subsidies will primarily benefit those nearing retirement—people who, unlike the young, have had their whole lives to save for their health-care needs.

Bocefish said:49-State Analysis: Obamacare To Increase Individual-Market Premiums By Average Of 41%

One of the fundamental flaws of the Affordable Care Act is that, despite its name, it makes health insurance more expensive. Today, the Manhattan Institute released the most comprehensive analysis yet conducted of premiums under Obamacare for people who shop for coverage on their own. Here’s what we learned. In the average state, Obamacare will increase underlying premiums by 41 percent. As we have long expected, the steepest hikes will be imposed on the healthy, the young, and the male. And Obamacare’s taxpayer-funded subsidies will primarily benefit those nearing retirement—people who, unlike the young, have had their whole lives to save for their health-care needs.

http://en.wikipedia.org/wiki/Manhattan_Institute_for_Policy_ResearchThe Manhattan Institute received over $31 million in grants from 1985 to 2012, from foundations such as the Koch Family Foundations

Regardless of the accuracy of the analysis, it spoke to the experience of a small minority of Americans, and it did not factor in the subsidies that will cushion some people from increased premiums.

Loyal Obama Supporters, Canceled by Obamacare

by Charles Ornstein

Nov. 6, 2013, 9:57 a.m.

http://www.propublica.org/article/loyal ... -obamacare

Lee Hammack and his wife JoEllen Brothers (Photo courtesy of Lee Hammack)

San Francisco architect Lee Hammack says he and his wife, JoEllen Brothers, are “cradle Democrats.” They have donated to the liberal group Organizing for America and worked the phone banks a year ago for President Obama’s re-election.

Since 1995, Hammack and Brothers have received their health coverage from Kaiser Permanente, where Brothers worked until 2009 as a dietitian and diabetes educator. “We’ve both been in very good health all of our lives – exercise, don’t smoke, drink lightly, healthy weight, no health issues, and so on,” Hammack told me.

The couple — Lee, 60, and JoEllen, 59 — have been paying $550 a month for their health coverage — a plan that offers solid coverage, not one of the skimpy plans Obama has criticized. But recently, Kaiser informed them the plan would be canceled at the end of the year because it did not meet the requirements of the Affordable Care Act. The couple would need to find another one. The cost would be around double what they pay now, but the benefits would be worse.

“From all of the sob stories I’ve heard and read, ours is the most extreme,” Lee told me in an email last week.

I’ve been skeptical about media stories featuring those who claimed they would be worse off because their insurance policies were being canceled on account of the ACA. In many cases, it turns out, the consumers could have found cheaper coverage through the new health insurance marketplaces, or their plans weren’t very good to begin with. Some didn’t know they could qualify for subsidies that would lower their insurance premiums.

So I tried to find flaws in what Hammack told me. I couldn’t find any.

The couple’s existing Kaiser plan was a good one.

Their new options were indeed more expensive, and the benefits didn’t seem any better.

They do not qualify for premium subsidies because they make more than four times the federal poverty level, though Hammack says not by much.

Hammack recalled his reaction when he and his wife received a letters from Kaiser in September informing him their coverage was being canceled. “I work downstairs and my wife had a clear look of shock on her face,” he said. “Our first reaction was clearly there’s got to be some mistake. This was before the exchanges opened up. We quickly calmed down. We were confident that this would all be straightened out. But it wasn’t.”

I asked Hammack to send me details of his current plan. It carried a $4,000 deductible per person, a $40 copay for doctor visits, a $150 emergency room visit fee and 30 percent coinsurance for hospital stays after the deductible. The out-of-pocket maximum was $5,600.

This plan was ending, Kaiser’s letters told them, because it did not meet the requirements of the Affordable Care Act. “Everything is taken care of,” the letters said. “There’s nothing you need to do.”

The letters said the couple would be enrolled in new Kaiser plans that would cost nearly $1,300 a month for the two of them (more than $15,000 a year).

And for that higher amount, what would they get? A higher deductible ($4,500), a higher out-of-pocket maximum ($6,350), higher hospital costs (40 percent of the cost) and possibly higher costs for doctor visits and drugs.

When they shopped around and looked for a different plan on California's new health insurance marketplace, Covered California, the cheapest one was $975, with hefty deductibles and copays.

In a speech in Boston last week, President Obama said those receiving cancellation letters didn’t have good insurance. “There are a number of Americans — fewer than 5 percent of Americans — who've got cut-rate plans that don’t offer real financial protection in the event of a serious illness or an accident,” he said.

“Remember, before the Affordable Care Act, these bad-apple insurers had free rein every single year to limit the care that you received, or use minor preexisting conditions to jack up your premiums or bill you into bankruptcy. So a lot of people thought they were buying coverage, and it turned out not to be so good.”

What is going on here? Kaiser isn’t a “bad apple” insurer and this plan wasn’t “cut rate.” It seems like this is a lose-lose for the Hammacks (and a friend featured in a report last month by the public radio station KQED.)

I called Kaiser Permanente and spoke to spokesman Chris Stenrud, who used to work for the U.S. Department of Health and Human Services. He told me that this was indeed a good plan. Patients in the plan, known as 40/4000, were remarkably healthy, had low medical costs and had not seen their premiums increase in years. “Our actuaries still aren’t entirely sure why that was,” he said.

While many other insurance companies offered skimpier benefits, Stenrud said, “our plans historically have been comprehensive.”

Kaiser has canceled about 160,000 policies in California, and about one third of people were in plans like Hammack’s, Stenrud said. About 30,000 to 35,000 were in his specific plan.

“In a few cases, we are able to find coverage for them that is less expensive, but in most cases, we’re not because, in sort of pure economic terms, they are people who benefited from the current system ... Now that the market rules are changing, there will be different people who benefit and different people who don’t.”

“There’s an aspect of market disruption here that I think was not clear to people,” Stenrud acknowledged. “In many respects it has been theory rather than practice for the first three years of the law; folks are seeing the breadth of change that we’re talking about here.”

That’s little comfort to Hammack. He’s written to California’s senators and his representative, House Minority Leader Nancy Pelosi, D-Calif., asking for help.

“We believe that the Act is good for health care, the economy, & the future of our nation. However, ACA options for middle income individuals ages 59 & 60 are unaffordable. We’re learning that many others are similarly affected. In that spirit we ask that you fix this, for all of our sakes,” he and Brothers wrote.

Jon Stewart: Obama 'Somewhat Dishonest' About Healthcare But Republicans Are 'Lying Like Motherf*ckers'

As far as i understand it if you've made zero the past year you do NOT have to sign up for it. Nor would you get any subsidies anyway. I'm in the same situation. I haven't even gone to look at the joke that is that website.BloodRed87 said:Serious question here. I've been unemployed since 2007 and stopped collecting unemployment benefits in 2010, do I still have to sign up for this bullshit healthcare to avoid being fined or am I exempt? Thanks.

BloodRed87 said:Serious question here. I've been unemployed since 2007 and stopped collecting unemployment benefits in 2010, do I still have to sign up for this bullshit healthcare to avoid being fined or am I exempt? Thanks.

BloodRed87 said:Serious question here. I've been unemployed since 2007 and stopped collecting unemployment benefits in 2010, do I still have to sign up for this bullshit healthcare to avoid being fined or am I exempt? Thanks.